The bad news is, you can’t achieve financial freedom just by your monthly savings. Or at least “financial freedom” in its truest and best sense — freedom of time and money. You could save monthly and wait until you’re 65, or you could choose to apply this mindset shift. The good news is, frugality and budgeting are skills that go beyond a household. When done right, it’ll also do wonders for your business and real estate investments.

(If you’re struggling with household budgeting, I have a piece on Kakeibo: The Japanese Budgeting System.)

Page Contents

Time is scarce, money is abundant

I am not a blind idealist that thinks everything will be fine, that starting a business or investing in real estate are easy decisions to make. There are real risks plus true freedom will require hard work. On most days you’ll have to gut it out.

And the challenges aren’t even just about business decisions. Sometimes you find yourself questioning your choice. When I stopped being an employee and started running a business, friends would ask how I was.

I made them believe I was in a better place, not truly believing it myself.

An epiphany

I’m in my mid-30s now and feel like it’s the perfect time to write about this. I’ve spent about half of my adult life working in corporate finance and the other half as a business owner. I like to think I genuinely understand both sides.

From an underpaid-overworked employee to earning six-figures in salary, and from a struggling business to a business that runs by itself, I am fortunate to have tried it all. And this is what I’ve realized.

Time is scarce but money is abundant.

You can always get more money, but you’ll never have your time back.

If you are after true financial freedom, there is no other way. Staying in corporate finance meant financial security at the expense of time. But that security was twofold. It also secured me to a life of working the 9-5. It meant waking up even when I didn’t want to. Missing important life events was a pattern.

Financial freedom through passive income

Entrepreneurship was actually forced on me and, especially with the benefit of hindsight, I’m glad it was. Financial security was no longer there but it also meant I had greater control of my life. Once we got our business running on autopilot, it was more free time. Free time to build another income stream and do it again. It hasn’t been all roses and COVID has made it doubly hard. But because the foundation has been built, it’ll be easier to scale. That’s the thing, you only learn and get better as you move along the journey.

Active income (salary) vs passive income

If you’re paid Php200,000/month by your employer, that’s essentially your ceiling. It’ll take you 8 hours a day and some overtime to earn that income. That’s not even counting the taxes withheld.

But if you’re able to establish a business that generates Php50,000 on autopilot, and maybe invest in real estate that generates Php50,000 with minimal effort, replicating that twice will earn you the same amount of money — and you’re not bounded by replicating it twice. You can repeat the process over and over, as long as you have the proper systems in place (but that’s admittedly easier said than done).

A common maxim loosely translated for us Filipinos says:

Php10,000 in passive income is more powerful than Php100,000 in active income.

Passive income is repeatable and scalable, from hundreds of thousands to billions. Active income is limited by the hours you work for it.

Nowadays I am able to step back and reflect. I truly am in a better place — now believing it wholeheartedly. If time and money are direct tradeoffs, then why replace a scarce resource for one that’s in abundance? That’s like trading water for sand in the middle of a desert.

Monthly savings for financial freedom

This chart shows three individuals with starting salaries of Php10,000, Php50,000, and Php100,000. I’ve assumed their salaries increase by 3% per year and that their saving rate is 10%.

In 45 years, these three employees would’ve saved Php1 million, Php5.5 million, and Php11 million in absolute terms, respectively. Doubling the saving rate will double these and halving would do the opposite. Can we say they’ve achieved freedom? Say a low-risk secure investment yields 3% p.a., then your Php11 million gives out around Php27,500/month. Probably good enough for some to retire off of but remember they’d be 65 years old at this point.

Business and passive income

On the other hand, a business scales a lot faster. Let’s take for example a small business like loading for mobile phones. (This is a very simplified example for demonstration purposes.) If you use an e-wallet like GCash or PayMaya (see my post on digital banks), a Php100 load will cost you Php95. Stores typically sell this at Php105. This translates to a markup of Php10 and a return of around 10.5% — that is, earning Php10 on your Php95 investment is approximately 10.5%.

How significant is this? If you serve 35 customers per day, this translates to a profit of Php10,500 per month (Php10 per customer x 35 customers per day x 30 days) on your Php99,750 investment. In other words, you buy the customers’ load at Php99,750 (i.e., Php95/customer) and sell it for Php110,250 (Php105/customer) for a Php10,500 profit.

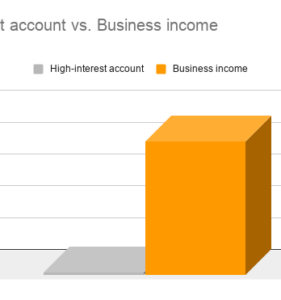

Assuming you do this for a year, serving 35 customers per day, your profit is Php10,500 per month x 12 months or Php126,000. Your initial investment of Php99,750 has earned Php126,000. Imagine earning Php126,000 on your Php99,750 deposit in a bank — laughable, right? The business route is head and shoulders above the monthly savings route for financial freedom. Here’s what the difference looks like in a graph.

Again, it’s not about the loading business and I am not advocating for it specifically. Think about how much the clothes you buy on Shopee costs the seller? Or when a YouTuber takes a full week to finish a video that earns them income for years?

Granted, these are very simplified examples. I have not considered the costs of setting up a store, hiring people, the risk that customers might not come, and a lot more. I’ve also not considered the upside such as growth potential from reinvesting your earnings.

But the point remains, margins in a business are substantially greater than interests earned on savings. Sure, a salary is paid monthly, but these examples also demonstrate how scalable a business is. You could do a lot more when you have the systems and infrastructure.

MJ DeMarco said it best in his book, Millionaire Fastlane. This was the (non-verbatim) message: If living from paycheck-to-paycheck is the sidewalk and running a business on autopilot is the fast lane, then saving regularly in hopes of a better future is the slow lane.

It’s better than the sidewalk, but slow nonetheless. And being slow wastes this scarce resource called time.

Should you quit your job?

Like I said, it’s not all roses and butterflies. You have to put in the effort. Running a business or buying real estate is hard work! For most people, it means even more hours upfront than working a regular job. I also recognize and appreciate that some prefer the security of a job and that monthly savings for financial security are their preferred choices. But there could be a happy medium between starting a business and settling at a job.

You could perhaps begin a side hustle and work from there. Save up money and build confidence before quitting your job. Unless you have a million-dollar idea and have the capacity to execute it, this is probably a good compromise. You could also partner with people who have the time and skills, although partnering with people is a very tricky topic that deserves its own post.

These are all valid options as long as you don’t forget what the end-goal is. But be warned that these also create comfort and may ultimately hinder progress. You are either spreading yourself out too thin rather than focusing on one (side hustle), or your progress is dependent on someone else rather than yourself (partnerships).

(Related: Be careful with trying to balance a job with a side hustle. I still believe financial freedom while having a job is a paradox.)

There’s no best approach and your circumstances will dictate what’s prudent. My goal isn’t to convince you of one approach. Rather, it is to show you a path you might not have known. But it’s not your fault.

Society tells us to go to school, get a job, save money, and retire at 60.

Sometimes all it takes is a trigger. If it weren’t for my parents and boss, I probably would still be working the corporate ladder. I hope this post creates the same ripple in you. If you ask me, there is a better way than simply saving monthly. But it’s a decision you’ll have to make.

*This post may contain affiliate links. You can read my affiliate disclosure here, Terms & Conditions, #6 Links.

Read more, select a topic: